Note: The Community Foundation would like to thank Wayne Lewis, of Lewis Financial for providing the following article from the Fidelity Learning Center.

If you are looking to make a non-deductible donation to charity, you may want to consider a Qualified Charitable Distribution, or QCD.

If you are age 72 or older, IRS rules require you to take required minimum distributions (RMDs) each year from your tax-deferred retirement accounts.

A QCD is a direct transfer of funds from your IRA, payable directly to a qualified charity, as described in the QCD provision in the Internal Revenue Code. Amounts distributed as a QCD can be counted toward satisfying your RMD for the year, up to $100,000. The QCD is excluded from your taxable income. This is not the case with a regular withdrawal from an IRA, even if you use the money to make a charitable contribution later on. If you take a withdrawal, the funds would be counted as taxable income even if you later offset that income with the charitable contribution deduction.

Why is this distinction important? If you take the RMD as income, instead of as a QCD, your RMD will count as taxable income. This additional taxable income may push you into a higher tax bracket and may also reduce your eligibility for certain tax credits and deductions. To eliminate or reduce the impact of RMD income, charitably inclined investors may want to consider making a qualified charitable distribution (QCD).

For example, your taxable income helps determine the amount of your Social Security benefits that are subject to taxes. Keeping your taxable income level lower may also help reduce your potential exposure to the Medicare surtax.

Am I eligible for QCDs?

In prior years, the rules that permitted QCDs required reauthorization from Congress each year, and those decisions were sometimes made late in the calendar year. With passage of the Protecting Americans from Tax Hikes (PATH) Act of 2015, the QCD provision is now a permanent part of the Internal Revenue Code. This means you can plan your charitable giving and begin reviewing your tax situation earlier each year.

Tip: With the 2020 tax law changes, there’s 1 additional factor to consider: you may take advantage of the higher standard deduction ($12,400 for single filers, $24,800 if married and filing jointly). This means that if you claim the standard deduction, you won’t be allowed to itemize things like charitable donations. However, since QCDs are not includable in income, the QCD is also not deductible. As such, the QCD can remain an option for your charitable giving, even if you claim the standard deduction in a given year.

The rules of QCDs

A QCD must adhere to the following requirements:

- You must be at least 70½ years old at the time you request a QCD. If you process a distribution prior to reaching age 70½, the distribution will be treated as taxable income.

- For a QCD to count toward your current year’s RMD, the funds must come out of your IRA by your RMD deadline, which is generally December 31 each year.

- Funds must be transferred directly from your IRA custodian to the qualified charity. This is accomplished by requesting your IRA custodian issue a check from your IRA payable to the charity. You can then request that the check be mailed to the charity or forward the check directly to the charity yourself.

Note: If a distribution check is made payable to you, the distribution would NOT qualify as a QCD and would be treated as taxable income.

- The maximum annual distribution amount that can qualify for a QCD is $100,000. This limit would apply to the sum of QCDs made to one or more charities in a calendar year. If you’re a joint tax filer, both you and your spouse can make a $100,000 QCD from your own IRAs.

- The account types that are eligible for QCDs include:

- Traditional IRAs

- Inherited IRAs

- SEP IRA (inactive plans only*)

- SIMPLE IRA (inactive plans only*)

- Under certain circumstances, QCDs may be made from a Roth IRA. Roth IRAs are not subject to RMDs during your lifetime, and distributions are generally tax-free. Consult a tax advisor to determine if making a QCD from a Roth is appropriate for your situation.

- Certain charities are not eligible to receive QCDs, including donor-advised funds, private foundations, and supporting organizations. You are not allowed to receive any benefit in return for your charitable donation. For example, if your donation covers your cost of playing in a charitable golf tournament, your gift would not qualify as a QCD.

NOTE: Though a QCD may not be placed directly into your donor-advised fund, The Community Foundation can still accept the QCD, place it in a holding fund, and distribute qualified grants based on your recommendations.

- Contributing to an IRA may result in a reduction of the QCD amount you can deduct.*

Tax filing for QCDs

A QCD is reported by your IRA custodian as a normal distribution on IRS Form 1099-R for any non-Inherited IRAs. For Inherited IRAs or Inherited Roth IRAs, the QCD will be reported as a death distribution. You should keep an acknowledgement of the donation from the charity for your tax records. Please consult a tax advisor to learn more.

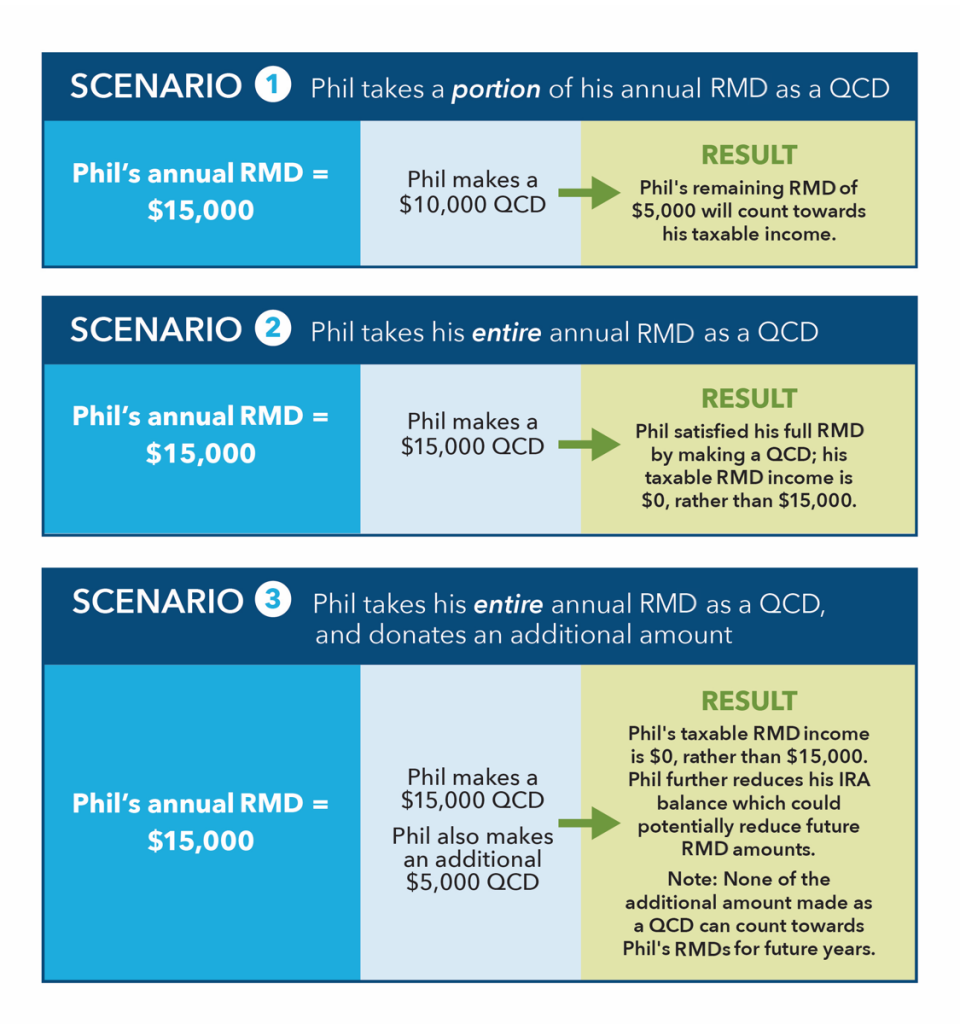

For a better understanding of how QCDs can affect your taxable income, let’s consider a few hypothetical scenarios. Phil has been taking RMDs for the past few years, but this year he has decided to make a QCD. Phil did not make any non-deductible contributions to his IRA, so all of his distributions would be taxable:

If you are 72, own an IRA, and donate to charity, QCDs may make sense for you; consult a tax advisor regarding your specific situation.