The pandemic has been difficult on all organizations whether it be higher demand for services or having to close their doors. Over the past couple of years The Community Foundation has been asked by both donors and nonprofit leaders to share tips on how to support their favorite organizations. Below are following are five evergreen options for supporting nonprofits compiled by our very own Cassandra Wagner Kartashov, Director of Grants and Programs here at The Community Foundation.

1 Unrestricted Gifts

Did you know that before the pandemic only 20% of funding for nonprofits in the United States had any degree of flexibility? Unrestricted gifts provide nonprofits with the ability to adapt to changing needs which has been more important than ever during the pandemic and will continue to be a need moving forward.

““…what we learned from the disaster was to trust the nonprofits to judge where they need to spend the funding” – Grantmaking Committee Member

2 Volunteer

Volunteerism is a tremendous resource as many nonprofits would not be able to conduct programs, raise funds or serve clients. Volunteering can also have positive impact on the volunteers mental health. If you are interested in volunteering you can contact your favorite nonprofit or check out Volunteer SLO for opportunities.

3 Give Grace

Nonprofits are usually understaffed even in the best of times. “The Great Resignation” has had a huge impact on local organizations. This may mean that your gift acknowledgement may not arrive in a timely manner or that the email you sent over a week ago has not been responded to. I recently heard from a beloved nonprofit leader that one of her donors decided to not make contributions to the organization any more after a new staff member failed to “properly greet” the donor. During these difficult times please remember to give a little extra grace.

4 Boost Morale

These past couple of years have been difficult on everyone. Our Board recently started provided treats for staff on multiple occasions which had a huge impact on staff morale and productivity. You’d be amazed by what a box of cupcakes can do to lift spirits.

5 Appreciation

I recently spoke with a nonprofit CEO who shared that she has one donor that writes a letter of appreciation with each gift they make to the organization. She shares the thank-you card with staff and then keeps them in a little box for days when she needs a pick-me-up. Letters of encouragement and thanks are validation of their hard work.

Note: The Community Foundation would like to thank Wayne Lewis, of Lewis Financial for providing the following article from the Fidelity Learning Center.

If you are looking to make a non-deductible donation to charity, you may want to consider a Qualified Charitable Distribution, or QCD.

If you are age 72 or older, IRS rules require you to take required minimum distributions (RMDs) each year from your tax-deferred retirement accounts.

A QCD is a direct transfer of funds from your IRA, payable directly to a qualified charity, as described in the QCD provision in the Internal Revenue Code. Amounts distributed as a QCD can be counted toward satisfying your RMD for the year, up to $100,000. The QCD is excluded from your taxable income. This is not the case with a regular withdrawal from an IRA, even if you use the money to make a charitable contribution later on. If you take a withdrawal, the funds would be counted as taxable income even if you later offset that income with the charitable contribution deduction.

Why is this distinction important? If you take the RMD as income, instead of as a QCD, your RMD will count as taxable income. This additional taxable income may push you into a higher tax bracket and may also reduce your eligibility for certain tax credits and deductions. To eliminate or reduce the impact of RMD income, charitably inclined investors may want to consider making a qualified charitable distribution (QCD).

For example, your taxable income helps determine the amount of your Social Security benefits that are subject to taxes. Keeping your taxable income level lower may also help reduce your potential exposure to the Medicare surtax.

Am I eligible for QCDs?

In prior years, the rules that permitted QCDs required reauthorization from Congress each year, and those decisions were sometimes made late in the calendar year. With passage of the Protecting Americans from Tax Hikes (PATH) Act of 2015, the QCD provision is now a permanent part of the Internal Revenue Code. This means you can plan your charitable giving and begin reviewing your tax situation earlier each year.

Tip: With the 2020 tax law changes, there’s 1 additional factor to consider: you may take advantage of the higher standard deduction ($12,400 for single filers, $24,800 if married and filing jointly). This means that if you claim the standard deduction, you won’t be allowed to itemize things like charitable donations. However, since QCDs are not includable in income, the QCD is also not deductible. As such, the QCD can remain an option for your charitable giving, even if you claim the standard deduction in a given year.

The rules of QCDs

A QCD must adhere to the following requirements:

You must be at least 70½ years old at the time you request a QCD. If you process a distribution prior to reaching age 70½, the distribution will be treated as taxable income.

For a QCD to count toward your current year’s RMD, the funds must come out of your IRA by your RMD deadline, which is generally December 31 each year.

Funds must be transferred directly from your IRA custodian to the qualified charity. This is accomplished by requesting your IRA custodian issue a check from your IRA payable to the charity. You can then request that the check be mailed to the charity or forward the check directly to the charity yourself.

Note: If a distribution check is made payable to you, the distribution would NOT qualify as a QCD and would be treated as taxable income.

The maximum annual distribution amount that can qualify for a QCD is $100,000. This limit would apply to the sum of QCDs made to one or more charities in a calendar year. If you’re a joint tax filer, both you and your spouse can make a $100,000 QCD from your own IRAs.

The account types that are eligible for QCDs include:

Traditional IRAs

Inherited IRAs

SEP IRA (inactive plans only*)

SIMPLE IRA (inactive plans only*)

Under certain circumstances, QCDs may be made from a Roth IRA. Roth IRAs are not subject to RMDs during your lifetime, and distributions are generally tax-free. Consult a tax advisor to determine if making a QCD from a Roth is appropriate for your situation.

Certain charities are not eligible to receive QCDs, including donor-advised funds, private foundations, and supporting organizations. You are not allowed to receive any benefit in return for your charitable donation. For example, if your donation covers your cost of playing in a charitable golf tournament, your gift would not qualify as a QCD.

NOTE: Though a QCD may not be placed directly into your donor-advised fund, The Community Foundation can still accept the QCD, place it in a holding fund, and distribute qualified grants based on your recommendations.

Contributing to an IRA may result in a reduction of the QCD amount you can deduct.*

Tax filing for QCDs

A QCD is reported by your IRA custodian as a normal distribution on IRS Form 1099-R for any non-Inherited IRAs. For Inherited IRAs or Inherited Roth IRAs, the QCD will be reported as a death distribution. You should keep an acknowledgement of the donation from the charity for your tax records. Please consult a tax advisor to learn more.

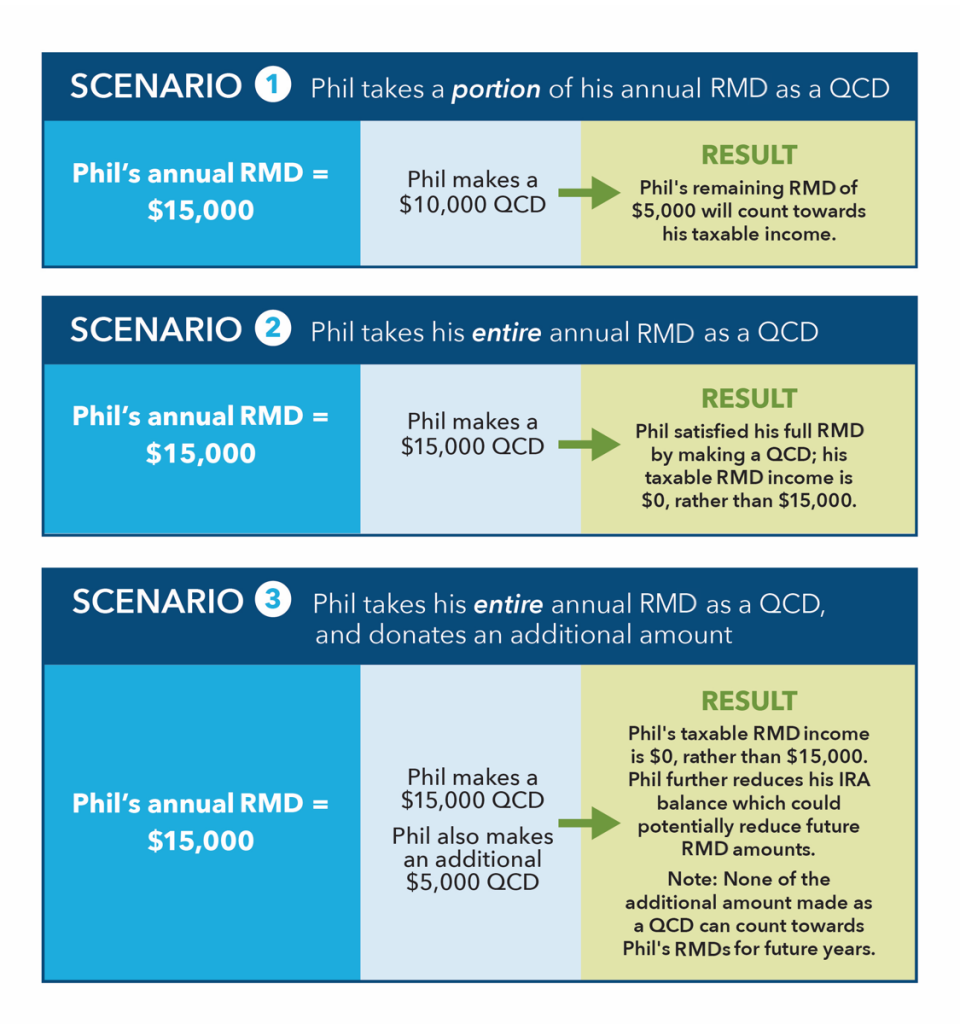

For a better understanding of how QCDs can affect your taxable income, let’s consider a few hypothetical scenarios. Phil has been taking RMDs for the past few years, but this year he has decided to make a QCD. Phil did not make any non-deductible contributions to his IRA, so all of his distributions would be taxable:

If you are 72, own an IRA, and donate to charity, QCDs may make sense for you; consult a tax advisor regarding your specific situation.

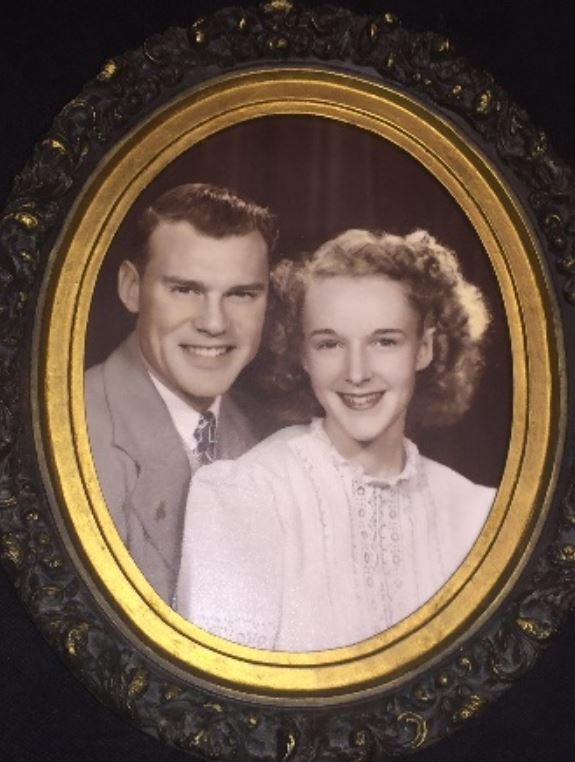

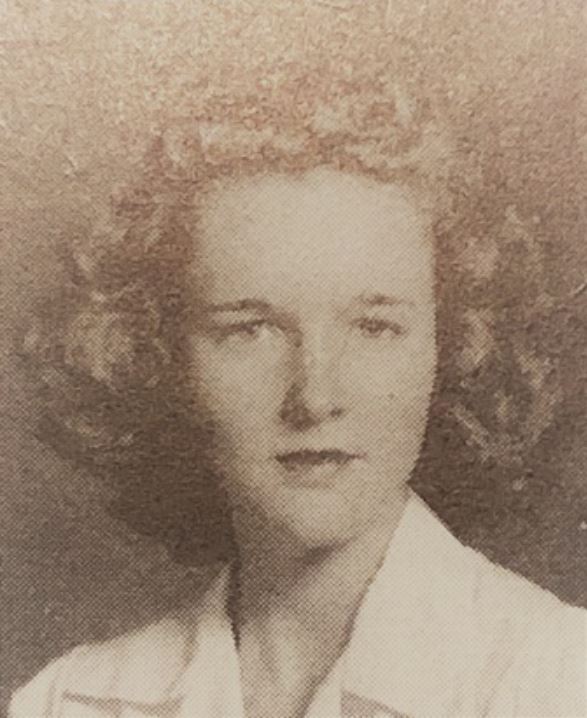

Bob and Pat Barlow loved living in San Luis Obispo County. Though they faced many misfortunes that kept many of their dreams from being realized, through hard work and frugality, they were able to save enough to live comfortably and to create a legacy that survives them. Many conversations with trusted advisors and close friends facilitated the planning needed to have a positive impact on the causes they cared about.

Pat was a child of the Depression. She was born in San Luis Obispo in 1928 into a family with no means. Her dream was to be the perfect wife, mother, and homemaker. Though at the time of her passing, she had no family close by, she did have wonderful friends and neighbors. One such person was the daughter of her close neighbors. They stayed close for decades as the daughter cared for her parents through their own decline. A deep mutual admiration formed. When the neighbors’ daughter was in her twenties, the Barlows asked her to be an “executor of last resort” and she agreed. Besides, what were the odds that all of those ahead on the list would be gone by the time she was needed?

By 2015, it became clear that Pat’s decades of planning paid off. The Executor helped Pat find a fiduciary in SLO to serve as backup, a trusted financial advisor protected her and her assets, and her longtime estate attorney made small revisions to refine her last wishes. While The Community Foundation was always a beneficiary, Pat realized that rather than supporting large national organizations, she could create a more personally meaningful impact by supporting local agencies addressing issues that concerned her, rather than contributing to large national organizations. She wanted to help people in the place she loved, especially those who faced some of the same challenges.

Pat and her Executor were attracted to the variety of options offered by The Community Foundation. They appreciated that a trusted local partner would evaluate the recipients and present the best choices based on local need and Pat’s intentions. Bob and Pat would be happy to know that the fruits of their hard work are making a difference in their community. And the Executor feels deeply honored to serve as a link between Bob and Pat and the programs being supported. Having known Pat for more than 50 years, it was an emotional moment when she was able to see the Barlows’ values given new life.

As the Executor shared, “The flexibility is tremendous, the fee structure is reasonable, and the personalization and care with which [The Community Foundation] continues to engage with me, makes this a wonderful relationship, not just a transaction.”